Hidden Costs of Canceling Car Insurance by State

Transportation in the United States has decreased significantly since mid-March when social distancing measures across the country first went into effect. With the closure of nonessential businesses and stay-at-home or shelter-in-place orders across the country, many drivers have found themselves with significantly fewer miles to drive each day – or in some cases, with none. Many may be tempted to cancel their auto insurance policy, under the erroneous assumption that this is the most cost-effective course of action.

Yet, canceling one’s auto insurance policy is full of hidden costs. Drivers who cancel their auto insurance policy without turning in their license and registration to the Department of Motor Vehicles can face serious consequences. Specifically, these drivers are unable to benefit from a prior insurance discount, and they also are required to pay insurance lapse fees to their DMV. Moreover, driving without car insurance is illegal in all states except for New Hampshire (Virginia is another exception, where drivers must pay a $500 uninsured motor vehicle fee to the Department of Motor Vehicles for permission to drive without insurance). Failure to produce proof of insurance can result in hefty fines, possible jail time, classification as a high-risk driver, and a further increase in insurance premiums.

{kind=link}

Insights

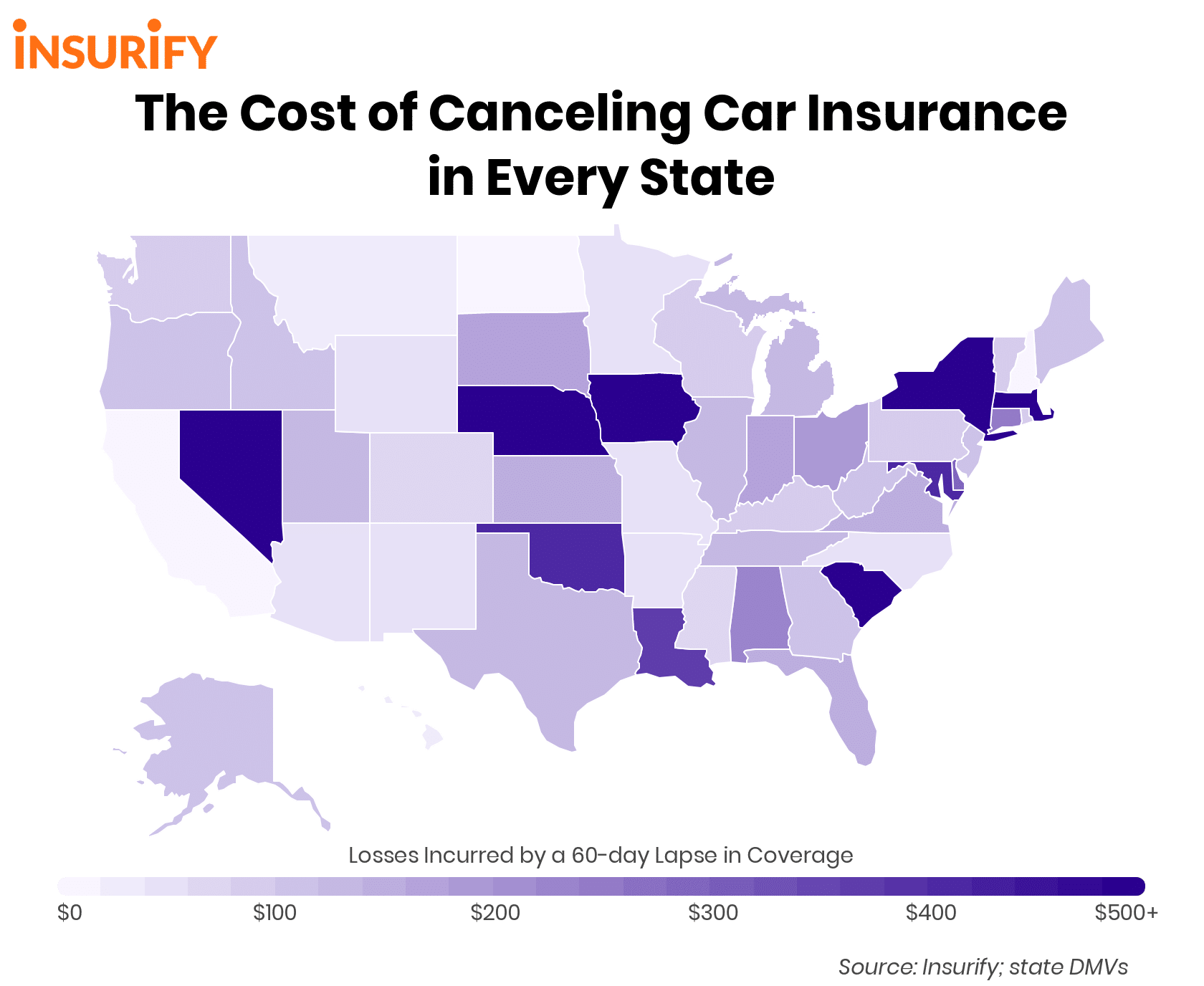

- Average cost in dollars. Averaged across all states, the long-term cost of a 60-day lapse in insurance coverage is $178: $21 from any prior insurance discount lost and $157 from DMV insurance lapse fees. For those caught driving uninsured, the average cost of a 60-day lapse in coverage jumps to $841: $521 from fines, and $142 from insurance penalties.

- Average percent increase. Nationally, the cost of a 60-day lapse in coverage costs drivers the equivalent of an additional 23 percent of their current policy, from DMV insurance lapse fees and lost prior insurance discounts. If caught driving without insurance, the average American driver can expect to pay 157 percent more than their current policy.

- Highs and lows. The cost of a 60-day lapse in coverage varies widely by state. While drivers in some states lose upwards of $500, drivers in North Dakota lose the least. In fact, North Dakotans stand to lose only $14 from lost prior insurance discounts, because DMV insurance lapse fees are nonexistent for the first offense. Keep in mind, however, that drivers in North Dakota must still pay $150 minimum in fines if caught driving uninsured.

Methodology

Insurify’s data science and research team calculated the cost of canceling auto insurance by state, based on a 60-day lapse in coverage. (Note that longer lapses in coverage can cost a driver significantly more in fees – and also can increase the risk of being caught if driving uninsured). Factors influencing the cost of canceling one’s policy include the opportunity cost of prior insurance discounts, as well as DMV reinstatement fees for a lapse in coverage. Further costs are incurred if drivers are caught uninsured, the consequences of which include fines, possible jail time, and an additional hike in insurance premiums.

To calculate the cost of a 60-day lapse in auto insurance coverage, Insurify’s data science and research team referred to data from public filings. The costs displayed here are based on aggregations of sample rates for four driver profiles that included varied gender, ages, driving histories, credit, marital statuses, prior insurance, higher education, employment, and military service. From these, they calculated the average annual cost of auto insurance in each state, based on data reflecting insurance premiums from over 100 providers. Following this, they broke down the average savings lost per insurer and state when the prior insurance discount is removed. Insurance lapse fee amounts were collected from the DMV of each state.

Fines for driving uninsured and additional increases in insurance premiums were not factored into state rankings due to the decrease in driving across all states at this time. Data on these penalties, including fines and jail time, was gathered from state government websites. Additional yearly insurance costs for drivers caught were calculated based on

States with the Highest Cost of Canceling Car Insurance

10. Delaware

- Cost of a 60-day lapse in coverage: $282

- Fine for uninsured driving violation: $1500-2000

- Additional (yearly) insurance cost increase after uninsured driving violation: $250

Delaware ranks tenth in the nation for the most expensive consequences of owning a vehicle without insurance, even if drivers are lucky enough to avoid getting caught driving uninsured. For those who are not so lucky, heavy fines of $1500 to $2000 are in the cards, as is a further $272 increase in insurance premiums. Other consequences of driving uninsured in Delaware include registration suspension, license suspension, and confiscation of plates.

9. Louisiana

- Cost of a 60-day lapse in coverage: $367

- Fine for uninsured driving violation: $175

- Additional (yearly) insurance cost increase after uninsured driving violation: $225

Drivers in Louisiana stand to lose a substantial amount of money for a 60-day lapse in insurance coverage. DMV fees make up about two-thirds of the cost while losing the opportunity to use a prior insurance coverage discount makes up the other third. And the Sugar State is by no means sweet to those who are caught driving uninsured: driving without insurance results in a fine of $175, up to 30 days of jail time, confiscation of plates, and an impounded car.

8. Maryland

- Cost of a 60-day lapse in coverage: $406

- Fine for uninsured driving violation: $1,000

- Additional (yearly) insurance cost increase after uninsured driving violation: $360

Canceling auto insurance is by no means free in the Free State. Maryland drivers do lose out on a small prior insurance discount, but primarily, they face hefty DMV fees for a lapse in insurance, which increase by $7 for each uninsured day after the first month. If caught driving uninsured, drivers risk six months of jail time, registration suspension, confiscation of plates, and five points on their driving record.

7. Oklahoma

- Cost of a 60-day lapse in coverage: $408

- Fine for uninsured driving violation: $250

- Additional (yearly) insurance cost increase after uninsured driving violation: $400

Those with a 60-day lapse in car insurance, but who are not caught on the roads driving uninsured, lose only $8 in prior insurance discounts but $400 in insurance lapse fees. Although fines for those caught driving uninsured are only $250 — lower than those of most states — these incautious drivers face up to 30 days in jail, license suspension, confiscated plates, and an impounded car.

6. Iowa

- Cost of a 60-day lapse in coverage: $489

- Fine for uninsured driving violation: $250

- Additional (yearly) insurance cost increase after uninsured driving violation: $400

Despite not making the top five on the list, Iowa has some of the highest DMV insurance lapse fees of any other state, at $485. As if this fee were not persuasion enough to drivers considering canceling their policies, those who are actually caught driving without insurance risk an additional $250 in fines, not to mention plate confiscation and an impounded car.

5. Massachusetts

- Cost of a 60-day lapse in coverage: $500

- Fine for uninsured driving violation: $500

- Additional (yearly) insurance cost increase after uninsured driving violation: $500

Ranking fifth in the country for the highest cost of canceling insurance is Massachusetts. While drivers in Massachusetts do not receive a prior insurance discount, DMV insurance lapse fees are incredibly high in this state. The Bay State also has the longest maximum jail sentence (1 year) for driving uninsured out of any other state on this list and is by no means lenient with those who unwisely choose to drive uninsured.

4. Nebraska

- Cost of a 60-day lapse in coverage: $500

- Fine for uninsured driving violation: $1,000

- Additional (yearly) insurance cost increase after uninsured driving violation: $500

The cost of canceling insurance in Nebraska is particularly severe. With a $500 DMV insurance lapse fee, drivers may think twice about canceling their policy. And if this fee were not persuasion enough, those who are actually caught driving without insurance risk 6 months of jail time, registration suspension, license suspension, an SR-22, an additional $1,000 in fines, and a further $500 increase in insurance premiums with such a violation on their record.

3. Nevada

- Cost of a 60-day lapse in coverage: $514

- Fine for uninsured driving violation: $600-1,000

- Additional (yearly) insurance cost increase after uninsured driving violation: $501

When it comes to driving without insurance in Nevada, it’s best not to take a gamble. The Silver State penalizes uninsured drivers very severely. Drivers are automatically charged an insurance lapse fee of $251, in addition to fines that increase dramatically. The first 31-90 days will cost a driver $250, then $500 for 91 to 180 days, and then $1,000 for more than 181 days. Those caught on the roads uninsured face an additional $600-1,000 in fines and a further $500 increase to their auto insurance, not to mention registration suspension, license suspension, confiscation of plates, car impoundment, and an SR-22.

2. New York

- Cost of a 60-day lapse in coverage: $576

- Fine for uninsured driving violation: $150-1500

- Additional (yearly) insurance cost increase after uninsured driving violation: $540

New York ranks second in the nation for some of the costliest consequences of canceling auto insurance. Drivers face DMV penalties that increase with each day: $8 per day for the first 30 days increases to $10 per day for the second 30 days, and then $12 per day for each day thereafter. For a 60-day lapse in coverage, this totals to $540. If caught driving uninsured, drivers risk added fines of $150-$1500, a $500 increase in insurance premiums, not to mention up to 15 days of jail time, registration suspension, license suspension, and an impounded car.

1. South Carolina

- Cost of a 60-day lapse in coverage: $790

- Fine for uninsured driving violation: $825

- Additional (yearly) insurance cost increase after uninsured driving violation: $750

Drivers in South Carolina allowing a lapse in their insurance coverage stand to lose the most compared to drivers in all other states. DMV insurance lapse fees make up most of this cost, at a whopping $750, while the opportunity cost of a prior insurance discount makes up $40. Those caught driving uninsured risk losing an additional $1,245 in fines and other DMV fees, in addition to registration suspension, license suspension, confiscation of plates, and an SR-22.

If you have questions or comments about this article, please contact insights@insurify.com.

More From My 103.5 FM